Why The Current System Produces These Outcomes - And Why Incremental Fixes Can't Solve Structural Failures

Five mechanisms that produce $5.3 trillion spending, 27 million uninsured, and $220 billion in medical debt - by design

This is the third in a series on fixing America’s healthcare system. In the first post, I outlined what a redesigned system looks like. In the second post, I showed the evidence that demands change. This post explains why the current system produces those outcomes - and why incremental fixes can’t solve structural failures.

In January 2026, executives from CVS Health, UnitedHealth Group, and Cigna testified before Congress for more than nine hours. Lawmakers asked a straightforward question: How does it benefit consumers when you own the insurance company, the pharmacy benefit manager that decides drug coverage, the pharmacies that dispense medications, the clinics where doctors prescribe them, and offshore shell companies that divert billions in manufacturer rebates?

The answer, delivered by CVS CEO David Joyner when asked if controlling Aetna insurance, CVS Caremark (managing 27% of all U.S. prescriptions), CVS pharmacies, Oak Street Health clinics, and Cordavis drug manufacturing represented “market concentration”: “I wouldn’t agree. It’s a model that works really well for the consumer.”

Rep. Alexandria Ocasio-Cortez responded: “I think it works really well for CVS.”

The hearings exposed something more fundamental than corporate greed. They revealed that the current healthcare system produces predictable outcomes not because companies behave badly, but because the structure rewards complexity, punishes transparency, and protects inefficiency. When regulators try incremental fixes-mandate rebate pass-through, ban spread pricing, require transparency - sophisticated actors create offshore entities, redefine terms, and technically comply while maintaining extraction.

The U.S. healthcare system doesn’t have a behavior problem. It has an architecture problem.

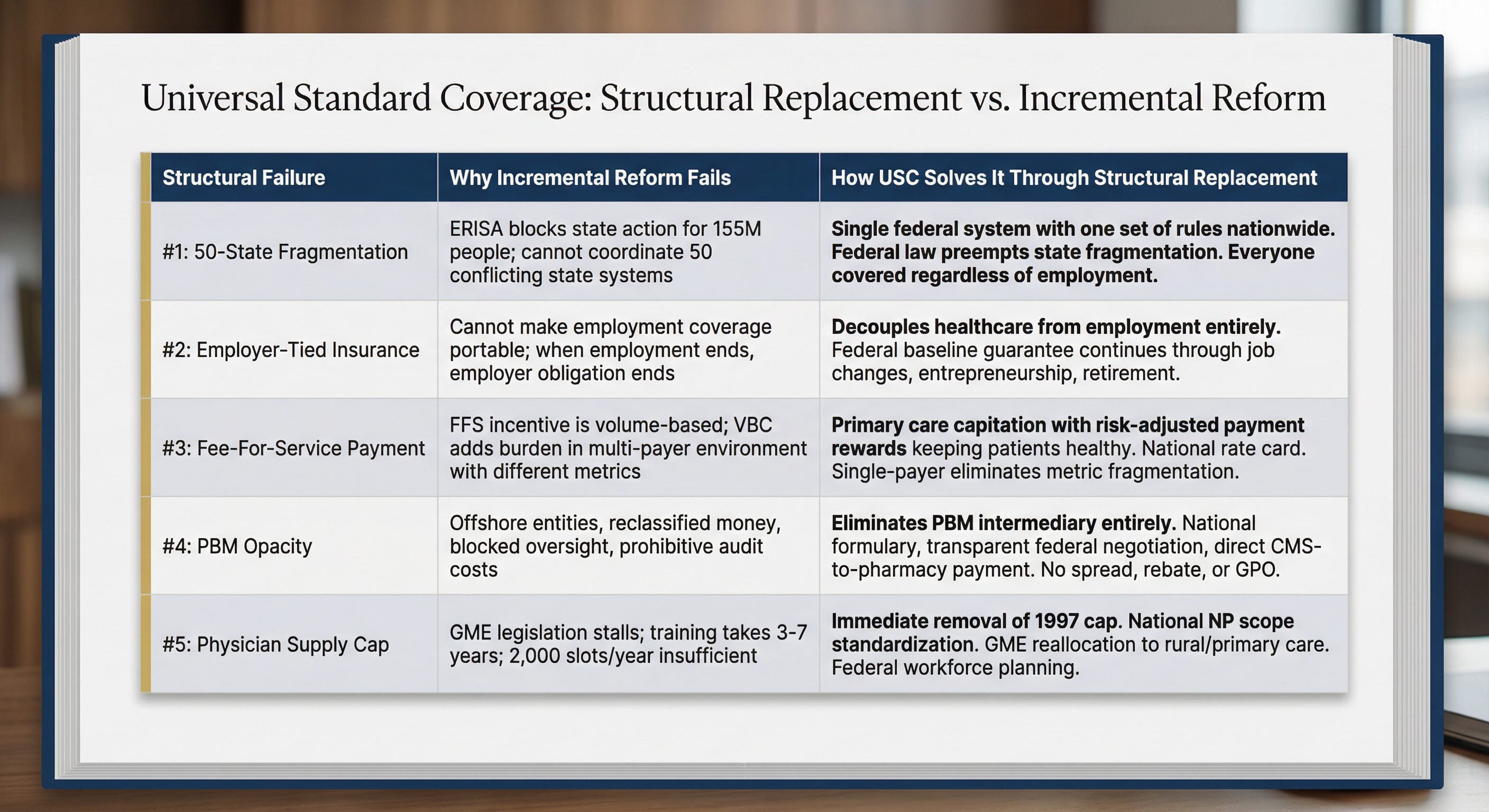

This section examines five structural mechanisms embedded in law, regulation, and market power. Each creates specific failures that incremental reform cannot fix. And each demonstrates why the Universal Standard Coverage (USC) proposal outlined in this series takes a fundamentally different approach: replacing the operating system rather than patching individual components.

About Universal Standard Coverage (USC)

Throughout this analysis, we reference how each structural failure relates to the Universal Standard Coverage proposal being advanced in this series. USC is a proposed federal healthcare financing system built on six core principles:

Healthcare as a baseline guarantee (not a luxury good or employment benefit)

One system, one set of rules (federal baseline, eliminating 50-state regulatory fragmentation)

$0 at point of care for medically necessary baseline services (no deductibles, copays, or surprise bills)

Frictionless operations (automated payment rails, minimal paperwork, clear patient statements)

Clinical decisions stay clinical (guided by doctors and evidence-based guidelines, not insurance company clerks)

Capitalism - compatible (private market remains for true extras and innovation, not for gatekeeping necessary care)

As we examine each structural failure below, we’ll show how it violates these principles - and why USC’s approach of structural replacement, rather than incremental reform, is necessary to solve problems that are embedded in the system’s architecture.

STRUCTURAL FAILURE #1: Fragmentation Across 50 State Regulatory Regimes

Why This Matters for USC: This fragmentation is precisely why USC proposes a single national system (Principle #2: One system, one set of rules) rather than trying to coordinate 50 different state approaches.

The Mechanism

The United States does not have one healthcare system. It has 50 state insurance regulatory regimes, plus a federal law that prevents states from regulating the health insurance that covers most working Americans.

This federal law - ERISA (Employee Retirement Income Security Act of 1974) - was originally passed to protect pension benefits. But it included a provision that prevents states from regulating employer-provided health insurance. At the time, this wasn’t controversial; employer insurance was straightforward. Today, ERISA means that 155 million Americans have health coverage that operates in a regulatory void: too “federal” for states to oversee, but with no federal agency actually regulating the insurance benefit terms.

The Data

The ERISA Preemption Problem:

155 million Americans have employer-sponsored coverage that states cannot regulate due to ERISA

Creates a “preemption vacuum”: no federal regulator sets standards, but states are blocked from enforcing their own

Multi-state employers must navigate 50 different regulatory frameworks for non-ERISA plans while ERISA plans operate with minimal oversight

When states try to reform healthcare, they can only reach the 45% of the population not covered by employer plans

State-by-State Variation in Basic Rules:

Nurse Practitioner scope of practice: 30 states allow full practice authority (NPs can see patients independently); 15 require reduced autonomy (some physician oversight); 11 require physician supervision (cannot practice independently)

Prior Authorization (PA) requirements - the insurance company approval process before treatment: Every state has different response time mandates, different thresholds for when approval is required, different transparency rules, and different data reporting requirements

10 states passed new PA legislation in 2024 alone - each with different standards for what counts as “timely” approval, creating a patchwork of requirements

Certificate of Need (CON) laws - state requirements for approval before building or expanding healthcare facilities: 38 states plus Washington D.C. maintain CON laws with completely different requirements; some require approval for new hospitals but not clinics, others the reverse

Essential Health Benefits - the services insurance must cover: Each state designates different “benchmark” plans as the standard; states change their benchmarks in different years with no coordination

Medical debt protections: More than half of states have not established financial protections for hospital patients such as mandatory payment plans or interest rate limits

Hospital market oversight: Utah exercises regulatory authority in only 1 of 11 possible oversight domains; Oregon exercises authority in 10 of 11 - creating vastly different competitive environments

Coordination of Benefits Complexity:

When a patient has coverage from multiple sources (for example, through their job and their spouse’s job, or through Medicare and a supplemental plan), “coordination of benefits” rules determine which insurer pays first. The National Association of Insurance Commissioners (NAIC) - a coordinating body for state regulators - published a model regulation, but states implement it differently. Some states coordinate only between group employer plans; others include individual coverage. Each state determines the order of payment priority. Multi-state families face different coordination rules depending on which state’s law applies.

Why This Creates Problems USC Would Solve

Problem 1: No Single Market Exists

A healthcare provider operating in multiple states must navigate 50 different regulatory frameworks. A patient moving from California to Texas faces different coverage standards, different rules about which providers can deliver care independently, different prior authorization requirements.

Under Universal Standard Coverage, a single federal system would replace state-by-state variation. One set of rules would apply nationwide: same coverage standards, same provider scope-of-practice rules, same payment system. This is USC Principle #2 (One system, one set of rules) in action.

Problem 2: Administrative Complexity Is Built Into the Structure

When coordination of benefits requires different calculations depending on which state’s rules apply, and when insurers must comply with 50 different sets of prior authorization laws, administrative costs multiply. Organizations managing national healthcare operations cannot implement single governance frameworks-they must accommodate varying state requirements.

Under USC, automated payment rails and a national rate card would eliminate coordination of benefits complexity entirely. There would be one payer (the federal system), one payment calculation, one set of rules. This is USC Principle #4 (Frictionless operations).

Problem 3: ERISA Blocks State Reform for 155 Million People

When states try to reform healthcare - requiring transparency from insurers, limiting out-of-pocket costs, mandating coverage of specific services - those reforms don’t apply to employer plans. ERISA preempts state law. The result: state reforms reach only 45% of the under-65 population.

Under USC, federal law would establish the baseline for everyone, eliminating the ERISA exemption issue. Everyone would have the same coverage guarantee regardless of employment status.

Why Incremental Fixes Fail

You cannot patch 50 state systems into one market:

ERISA is federal law. States cannot override it. Any state-level reform automatically excludes 155 million people in employer plans. Federal reform requires Congressional action but must navigate 50 state interests, each protecting their regulatory authority.

Regulatory arbitrage continues:

Companies domicile their operations in states with favorable regulations. Insurers structure plans to maximize ERISA preemption benefits. When one state requires transparency, companies shift operations to states that don’t.

Example from January 2026 hearings:

CVS, UnitedHealth, and Cigna each created offshore “Group Purchasing Organizations” - entities that negotiate drug rebates. CVS created Zinc Health Services (domiciled in Minnesota/Delaware). UnitedHealth created Emisar Pharma Services (purportedly in Ireland, though not registered in the Irish business database). Cigna created Ascent Health Services (headquartered in Switzerland). When states tried to regulate how much of manufacturer rebates these companies retained, the companies moved rebate negotiation to entities beyond U.S. state jurisdiction.

The structural reality:

You cannot create one national healthcare system by coordinating 50 state systems plus federal ERISA preemption. You must replace fragmentation with a single federal standard that applies to everyone.

STRUCTURAL FAILURE #2: Employer-Tied Insurance Locks In Inefficiency

Why This Matters for USC: This employment link is why USC proposes healthcare as a baseline guarantee independent of employment status (Principle #1), eliminating the structural cause of job lock and coverage gaps.

The Mechanism

In the United States, healthcare coverage is not a baseline guarantee. It is an employment benefit. When employment changes, coverage ends. This creates job lock (workers staying in jobs primarily to maintain health insurance), coverage gaps during transitions, massive administrative burden, and wage suppression as premium growth crowds out pay increases.

The Data

Job Lock - When Health Insurance Prevents Job Changes:

25% reduction in voluntary job turnover when workers have employer-provided insurance - from 16% to 12% annually, according to the foundational 1994 research by economist Brigitte Madrian published by the National Bureau of Economic Research (NBER)

580,000 parents became “job locked” by the Affordable Care Act’s dependent coverage mandate alone, according to 2024 research published in the Journal of Public Economics

Workers with employer insurance are 25-45% more likely to stay in unwanted jobs compared to those without employer coverage

This gap persists post-ACA: Those without employer insurance remain 25-45% more likely to switch jobs, meaning the Affordable Care Act’s marketplaces did not eliminate job lock

Coverage Gaps and COBRA:

When someone leaves a job, their employer coverage typically ends immediately or at the end of that month. COBRA (Consolidated Omnibus Budget Reconciliation Act) allows temporary continuation of employer coverage, but at full cost:

COBRA costs 4x the normal employee premium ($400-700/month per person) because the former employee must pay the full premium (what employer previously paid plus what employee paid) plus a 2% administrative fee

Creates an impossible choice during job transitions: pay unaffordable COBRA or go uninsured while searching for new coverage

Administrative Burden:

$21.6 billion annually spent by U.S. employees just coordinating with health insurance administration-time spent filing claims, resolving billing disputes, verifying coverage, navigating provider networks, understanding what is and isn’t covered

This is not medical care. This is pure administrative friction.

Wage Suppression:

American families lost $125,340 in cumulative wages (1988-2019) due to premium growth crowding out compensation, according to 2024 research published in JAMA Network Open

Health insurance premiums rose from 7.9% of total compensation (1988) to 17.7% (2019)

By 2019, premiums consumed 28.5% of compensation for families at the 20th percentile of earnings versus only 3.9% at the 95th percentile - a nine-fold disparity

Racial inequity compounds this: White families pay 13.8% of compensation in premiums versus 19.8% for Hispanic families and 19.2% for Black families

Why This Creates Problems USC Would Solve

Problem 1: Healthcare Is Not Guaranteed When It Depends on Employment

Job loss, entrepreneurship, retirement, caregiving, part-time work, gig work - all trigger coverage loss or force prohibitively expensive COBRA. Healthcare functions as an employment benefit, not a baseline right.

Under Universal Standard Coverage, coverage would be a federal guarantee independent of employment. Job change, starting a business, retiring early, taking time off for caregiving - coverage continues seamlessly. This is USC Principle #1 (Healthcare as a baseline guarantee).

Problem 2: Workers Pay Twice-And Still Face Gaps

Workers pay an average $6,850/year for family coverage (2025 Kaiser Family Foundation data), PLUS deductibles and copays when they use care, PLUS face coverage gaps during job transitions, PLUS pay 4x normal premium for COBRA if they need continuity.

Under USC, $0 at point of care for medically necessary baseline services means no premiums, no deductibles, no copays, no gaps, no COBRA crisis. This is USC Principle #3 ($0 at point of care).

Problem 3: $21.6 Billion in Pure Administrative Friction

When each employer chooses different insurance plans with different networks, different prior authorization requirements, different billing codes, and different claims processes, employees spend billions of hours navigating this complexity-time that could be spent working, caregiving, or living.

Under USC, automated payment rails would eliminate most of this friction. One system, one set of rules, clear patient statements. This is USC Principle #4 (Frictionless operations).

Why Incremental Fixes Fail

You cannot make employer insurance portable:

Employment-based coverage is fundamentally tied to employment status. When employment ends, the employer has no obligation to continue coverage. COBRA is not portability-it’s temporary continuation at a price most people cannot afford. True portability would require employers to continue subsidizing coverage for former employees indefinitely, which is not economically viable.

ACA marketplaces did not eliminate job lock:

The Affordable Care Act created insurance marketplaces where people without employer coverage can buy insurance. But data shows the 25-45% gap in job mobility persists between those with and without employer coverage. Why? Because marketplace premiums for equivalent coverage often exceed the subsidized premiums workers pay through employers, maintaining the financial lock-in.

Premium growth continues to crowd out wages:

Even with the ACA’s success in slowing healthcare cost growth (2010-2019), premiums rose 342% from 1999-2024 while wages rose only 119%. The gap is structural: when employers face 5-7% annual healthcare cost increases, they respond by limiting wage growth to stay within budget.

The structural reality:

You cannot make employer-tied insurance function as a baseline guarantee because coverage will always end when employment ends. The only solution is to decouple healthcare from employment entirely-which is what USC proposes.

STRUCTURAL FAILURE #3: Fee-For-Service Payment Drives Volume Over Value

Why This Matters for USC: This volume-over-value incentive is why USC proposes primary care capitation and a national rate card (Principle #5: Clinical decisions stay clinical), changing the financial reward from “do more” to “keep patients healthy.”

The Mechanism

Under fee-for-service (FFS) payment, healthcare providers are paid for each service delivered. More tests, more procedures, more visits equal more revenue. This creates financial pressure to maximize volume regardless of medical necessity. While some “value-based care” (VBC) programs attempt to reward quality, fee-for-service remains the dominant payment model in U.S. healthcare.

The Data

Unnecessary Medical Care - Physicians’ Own Assessment:

A Johns Hopkins University physician survey with 70.1% response rate, published in PLOS ONE, found that doctors believe:

20.6% of overall medical care is unnecessary

22% of prescription medications unnecessary

24.9% of medical tests unnecessary

11.1% of procedures unnecessary

$210 billion wasted annually on unnecessary services (National Academy of Medicine estimate)

229,000 unnecessary coronary stents implanted 2019-2021, costing Medicare $2.4 billion

106,474 unnecessary procedures performed March-December 2020 during the COVID-19 pandemic

The Primary Driver: Fear of Lawsuits

84.7% of physicians cite malpractice fear as the reason for over-treatment

Defensive medicine-ordering tests and procedures primarily to protect against potential lawsuits rather than for clinical benefit-costs $45.6-55.6 billion annually (2.4% of total U.S. healthcare spending)

13% of hospital costs are defensive medicine related ($226 per $1,695 patient admission)

28% of all hospital orders have some defensive component

$2 billion annually in defensive medicine for orthopedic surgery specialty alone ($100,000 per surgeon per year)

24% of all orthopedic tests ordered are for defensive reasons rather than clinical indication

Fee-For-Service Remains Dominant Despite Reform Efforts:

Nearly 40% of payments remain pure fee-for-service with no quality measure tied to payment (2020 data from Health Affairs)

Only 6.7% of payments are population-based (capitation or bundled payment where providers receive fixed payment to care for a patient population)

Despite more than a decade of Centers for Medicare & Medicaid Services (CMS) value-based care initiatives, FFS remains the default

Why This Creates Problems USC Would Solve

Problem 1: Financial Pressure Overrides Clinical Judgment

When 84.7% of physicians cite malpractice fear and 28% of hospital orders have a defensive component, clinical decisions are not being made on clinical grounds. They are being made to maximize revenue and minimize legal risk. The payment system creates misaligned incentives.

Under Universal Standard Coverage, primary care physicians would be paid through risk-adjusted capitation - a fixed per-member payment adjusted for how sick the patients are. This creates financial incentive to keep patients healthy through prevention and effective chronic care management, not to order more tests. This is USC Principle #5 (Clinical decisions stay clinical).

Problem 2: Prevention Is Not Reimbursed; Late-Stage Disease Is Highly Reimbursed

Under FFS, a primary care doctor spending 30 minutes counseling a diabetic patient on diet and exercise receives far less payment than an interventional cardiologist performing a cardiac catheterization on that same patient after years of uncontrolled diabetes lead to heart disease. The system financially rewards treating preventable late-stage complications over preventing them.

Under USC, PCP capitation would reward keeping patients healthy. A PCP whose diabetic patients have well-controlled blood sugar and avoid complications would be more financially successful than one whose patients progress to expensive late-stage interventions.

Problem 3: High-Margin Services Are Overused; Low-Margin Necessities Are Underused

FFS payment rates are higher for diagnostic imaging, procedures, and subspecialty consultations than for prevention, chronic care coordination, or time-intensive primary care. The payment system creates financial incentive to do more imaging and procedures, not to invest time in the unsexy work of keeping people healthy.

Under USC, a national rate card would set standardized payment rates that reward the services that actually improve health outcomes, not just the ones that generate revenue. This is USC Principle #6 (Capitalism-compatible-rewarding innovation and quality, not volume).

Why Incremental Fixes Fail

Value-based care has not replaced fee-for-service after more than a decade:

Why? Because value-based payment in a multi-payer environment requires:

Robust information technology infrastructure many smaller practices and rural hospitals cannot afford

Data collection and performance tracking that adds administrative burden and cost

Multi-year outcome windows that delay revenue recognition, creating cash flow problems for providers

Risk-adjustment methodologies that are complex, often gamed, and require sophisticated actuarial expertise

Other countries use fee-for-service but spend less:

Canada, France, and Germany all use FFS payment but spend 40-50% less per capita than the U.S. Why? Because they have:

Single-payer systems with rate regulation that prevent price inflation

Larger not-for-profit hospital sectors that remove the profit motive for volume

Different malpractice environments that reduce defensive medicine pressure

Incremental value-based care in a fragmented multi-payer system creates MORE administrative burden:

Every private insurer and government program has different quality metrics, different performance thresholds, different reporting requirements, different timelines. A physician practice participating in value-based contracts with five different payers must track five different sets of metrics, submit five different reports, and meet five different standards-all while still operating in an FFS environment for patients whose insurers don’t participate in VBC programs.

The structural reality:

You cannot make fee-for-service reward prevention over procedures because the fundamental incentive is volume. The only solution is to change the payment model to one that financially rewards keeping patients healthy-which requires a single payer who can implement capitation uniformly, not 50 different state systems plus hundreds of private insurers each with different approaches.

STRUCTURAL FAILURE #4: Pharmacy Benefit Managers Profit From Opacity - And Evade Every Regulatory Fix

Why This Matters for USC: This opacity and vertical integration is why USC proposes eliminating the PBM intermediary entirely (Principle #4: Frictionless operations and Principle #6: Capitalism-compatible), replacing it with direct federal negotiation and transparent pricing.

The Mechanism

Pharmacy Benefit Managers - companies commonly called PBMs - negotiate drug prices between pharmaceutical manufacturers and health insurance plans. In theory, PBMs use their purchasing power to negotiate lower drug costs. In practice, they operate as opaque intermediaries that extract billions through undisclosed price spreads, retained manufacturer rebates, and steering patients to their own affiliated pharmacies. When regulators mandate transparency or rebate pass-through, PBMs create offshore entities to retain the money under new labels before it can be classified as a “rebate.”

The Data

Market Concentration - Three Companies Control Drug Access:

80% of 270 million Americans’ prescription drug claims flow through just three PBMs:

Express Scripts (owned by Cigna): 30% market share

CVS Caremark (owned by CVS Health): 27% market share

OptumRx (owned by UnitedHealth Group): 23% market share

The Herfindahl-Hirschman Index (HHI) - a market concentration score where 0 means perfect competition and 10,000 means total monopoly-measures the PBM market at 1,972. The Federal Trade Commission considers anything above 1,800 to indicate a “highly concentrated market” that raises competitive concerns.

Revenue Extraction - Documented by Federal Investigators:

$7.3 billion in excess revenue (2017-2022) from specialty generic drug markups by the Big 3 PBMs - markups of hundreds to thousands of percent above what the drugs cost, according to Federal Trade Commission investigation

42% annual growth rate in PBM markup revenue from 2017-2021

$1.4 billion from spread pricing alone: PBMs charged health plans more than they reimbursed the pharmacies that dispensed the drugs, pocketing the difference (this is called “spread pricing”)

$223 billion in manufacturer rebates (2022) - manufacturers pay these rebates and discounts to PBMs in exchange for favorable placement on formularies (the lists of covered drugs), but PBMs are not required to disclose how much they retain versus pass through to health plans

$356 billion gross-to-net bubble (2024) - this is the gap between drug list prices and the net revenue manufacturers actually receive after all rebates, discounts, and fees. This $356 billion exists in the system as money changing hands between manufacturers, PBMs, insurers, and pharmacies in ways that are not transparent to patients or employers.

Patient cost-sharing rose $279 million in 2021 from PBM markups alone-when PBMs inflate costs, patients with coinsurance (paying a percentage of drug cost) pay more

Vertical Integration and Affiliated Pharmacy Capture:

68% of specialty drug dispensing revenue (2023) flows to pharmacies owned by the same company that owns the PBM, up from 54% in 2016

This is not market competition-it is steering patients to captive pharmacies for profit extraction

Example documented by the FTC: A cancer medication priced at $8,900 when processed through a traditional PBM versus $57 through a transparent pass-through model - an $8,843 difference for an identical drug

Opacity Mechanisms - How PBMs Hide Pricing:

Spread pricing: PBM negotiates $80 reimbursement rate with the pharmacy, bills the health plan $100, pockets the $20 spread - and does not disclose this spread to the plan sponsor

Rebate retention: Manufacturers pay rebates to PBMs; PBMs are not required to disclose how much they retain versus pass through to health plans or patients

Maximum Allowable Cost (MAC) lists: PBMs maintain secret lists of maximum reimbursement rates for generic drugs; neither plan sponsors nor pharmacies are told how drugs are added or removed from these lists or how the MAC is calculated

Reported profit margins are misleading: PBMs report 4-7% profit margins (among the thinnest in healthcare), but this doesn’t account for profits their affiliated pharmacies earn from the 68% of specialty drug revenue they capture

Audit costs are prohibitive: Professional PBM contract audits cost $15,000-200,000, preventing smaller employers from detecting overcharges

The January 2026 Offshore Shell Game - How PBMs Evade Rebate Reform

As regulatory pressure mounted to force PBMs to pass 100% of manufacturer rebates through to health plans, the Big 3 PBMs created separate companies called “Group Purchasing Organizations” or GPOs. These GPOs, domiciled offshore or in states with minimal oversight, negotiate the rebates with manufacturers and retain a portion as “administrative fees” BEFORE the remaining money is passed to the PBM and classified as a “rebate.” This allows PBMs to truthfully claim they pass through “100% of rebates” while their affiliated GPO retains billions upstream.

ZINC HEALTH SERVICES (affiliated with CVS Caremark):

Founded 2020, registered as an LLC in Delaware with operations in Minnesota

Physical presence: According to testimony from a former employee, Zinc occupies space inside the CVS Caremark building separated by a temporary wall; both entities report to the same vice president

No public phone number, no email address, skeleton staff

Illinois recovered $45 million from CVS Caremark for improperly retaining Zinc rebates that should have been passed to the state employee health plan; CVS settled immediately to avoid public disclosure

Louisiana recovering approximately $50 million through a settlement announced December 2025

CVS sued the state of Illinois to block Freedom of Information Act (FOIA) requests seeking documents about the Zinc arrangement

Contract language obtained in the Illinois lawsuit states that Zinc pays CVS Caremark “compensation for services rendered” from the money manufacturers pay to Zinc - meaning Zinc pays CVS to do the work that Zinc is supposedly doing independently

EMISAR PHARMA SERVICES (affiliated with OptumRx):

Founded 2021, supposedly domiciled in Ireland

Not registered in the Irish business database according to investigation by Hunterbrook Media

Physical presence: A Hunterbrook reporter visited the listed Dublin address during business hours and found a single empty room inside the Optum building with no one working there

No website, no public phone number, approximately 24 employees listed on LinkedIn

Job postings for Emisar positions are posted by UnitedHealth and Optum, not by Emisar as a separate entity

ASCENT HEALTH SERVICES (affiliated with Express Scripts):

Founded 2019, registered as an LLC in Delaware but headquartered in Switzerland

Physical presence: Small office in Switzerland; when a Hunterbrook Media reporter attempted to visit and investigate, the office called police

Negotiates rebates not only for Express Scripts but also for Prime Therapeutics (a separate PBM), creating additional market concentration

Part of an estimated $200 billion annually flowing through the three offshore GPOs

Congressional Investigation:

In August 2025, House Oversight Committee Chairman James Comer (R-Kentucky) sent formal investigative letters to all three companies. His letter stated: “GPOs create another layer of pricing opacity and complexity. This is especially true for GPOs headquartered overseas as these entities may be used to retain additional revenue and fees and to sidestep U.S. legislative and regulatory reforms.”

Why This Creates Problems USC Would Solve

Problem 1: The System Is Designed to Prevent Oversight

When audit costs are $15,000-200,000 per contract, when key contract terms are redacted in legal proceedings, when companies create offshore entities beyond state jurisdiction, and when companies sue states to block public records requests, opacity is not a side effect-it is the business model.

Under Universal Standard Coverage, there would be no PBM intermediary. The federal government would negotiate drug prices directly with manufacturers through a transparent process, publish the negotiated prices, and pay pharmacies directly to dispense medications. No spread to capture, no rebate to retain, no offshore entity to create. This is USC Principle #4 (Frictionless operations).

Problem 2: Vertical Integration Allows Margin Stacking at Every Step

When the same company owns the insurance plan, the PBM that determines which drugs are covered, the pharmacy that dispenses the drugs, and the GPO that negotiates manufacturer rebates, that company extracts profit at every transaction in the drug supply chain. The patient encounters the same company’s profit-taking at multiple steps.

Under USC, single-payer federal financing would eliminate insurer - PBM vertical integration. There would be one payer negotiating on behalf of all Americans, not three oligopolies each controlling their own vertically integrated supply chains. This is USC Principle #6 (Capitalism-compatible-markets for innovation, not toll-taking).

Problem 3: The $356 Billion Gross-to-Net Bubble Raises Costs for Patients

When manufacturers raise list prices to fund larger rebates that PBMs and insurers negotiate, patients with high-deductible plans or coinsurance (paying a percentage of drug cost) pay based on the inflated list price, not the net price after rebates. The rebate game raises costs for the patients most financially vulnerable.

Under USC, transparent negotiated pricing would establish the actual price paid, eliminating the gap between list price and net price. Patients would not encounter inflated list prices because there would be no price inflation needed to fund a rebate system.

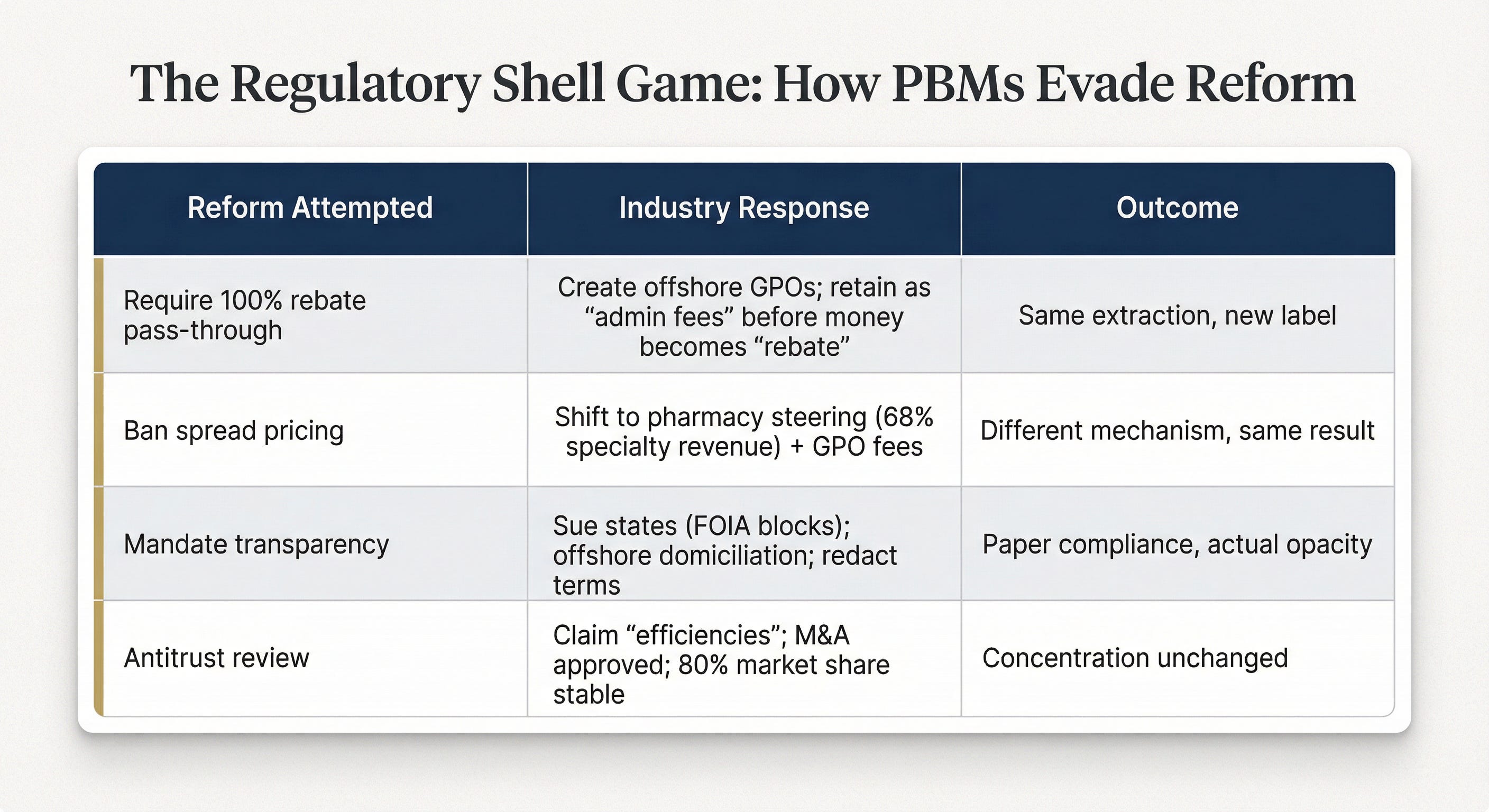

Why Incremental Fixes Fail: The Regulatory Shell Game

The January 2026 Congressional hearings revealed a pattern: for every regulatory fix, sophisticated actors create a workaround that technically complies while maintaining the same extraction.

Cigna’s “Rebate-Free” Model Announced October 2025:

Cigna announced it would “abandon traditional manufacturer rebates” starting 2027-2028, replacing them with “point-of-sale discounts.” This sounds like transparency reform. But analysis reveals:

Optional, not mandatory: Only applies to fully insured commercial employer plans that choose to opt in; Cigna expects only approximately 50% adoption by the end of 2028

Ascent Health Services (Swiss GPO) still operates: Nothing changes for the offshore entity that negotiates and retains fees upstream

Creates MORE opacity: Industry analysts note that “discount in lieu of rebates is now essentially impossible to track or audit”

Economic Liberties Project conclusion: “Cigna’s promise to abandon manufacturer rebates is a red herring. The policy change will help Cigna sidestep regulatory scrutiny of rebates while maintaining its major profit drivers: administrative fees, including those related to its Swiss subsidiary Ascent Health Services.”

The Smoking Gun from Zinc Contract:

In documents obtained through the Illinois lawsuit, the contract between Zinc and CVS Caremark states: “Company and GPO acknowledge and agree that a portion of the [Redacted] remitted by GPO to Company constitutes compensation for services rendered by Company to GPO.”

Translation: Zinc pays CVS Caremark to do the work that Zinc is supposedly doing. There is no functional separation. The GPO is a shell company created to retain rebate money under a different label.

The January 2026 Congressional Testimony

Rep. Alexandria Ocasio-Cortez to CVS CEO David Joyner:

> “Mr. Joyner, CVS Health owns Aetna insurance, CVS Caremark which manages 30% of all prescriptions in the United States, CVS pharmacies, Oak Street Health medical clinics, and the drug manufacturer Cordavis. This is quite a bit of market concentration. Wouldn’t you agree?”

Joyner’s response:

> “I wouldn’t agree. It’s a model that works really well for the consumer.”

Rep. Ocasio-Cortez:

> “I think it works really well for CVS.”

Rep. Greg Murphy (R-North Carolina):

> “You have put profits above patients. You have squarely abused your position of authority to deliver healthcare to patients in this country. This vertical integration has destroyed competition. These companies should be broken up.”

Rep. Jake Auchincloss (D-Massachusetts):

> “The big three health insurance corporations, knowing that PBM reform is around the corner, needed a different way to retain profits while still-on paper-complying with new requirements and the coming requirements of PBM reform.”

When lawmakers asked about GPO profits, the CEOs declined to provide specific figures.

The Structural Reality

You cannot make PBM opacity transparent through disclosure rules when:

Sophisticated actors create offshore entities beyond U.S. state jurisdiction

Audit costs are prohibitive for smaller employers

Contract terms are redacted even in legal proceedings

Companies sue states to block public information requests

Money can be reclassified from “rebates” to “administrative fees” paid to affiliated entities before it reaches the PBM

You cannot break up vertical integration when market concentration allows reconsolidating through mergers and acquisitions within a decade, and when the underlying multi-payer structure creates financial incentive for integration.

The only solution is to eliminate the intermediary layer entirely - which is what Universal Standard Coverage proposes. A national formulary with transparent pricing negotiated by a federal commission, direct payment from the single federal payer to pharmacies, no spread to capture, no rebate game to play, no offshore entity to create.

STRUCTURAL FAILURE #5: Artificial Physician Supply Constraints Create Bottlenecks

Why This Matters for USC: This federal cap on physician training is why USC proposes immediate removal of the 1997 cap plus national standardization of nurse practitioner scope of practice (Principle #1: Healthcare as baseline guarantee requires adequate provider supply).

The Mechanism

The United States artificially limits physician supply through a federally imposed cap on Medicare-funded residency positions. This cap-established in the Balanced Budget Act of 1997 - has remained largely frozen for 27 years, despite population growth, demographic aging, and projected shortages of 86,000-139,000 physicians by 2036. Because all medical school graduates must complete residency training to practice medicine in the United States, this cap functions as an absolute bottleneck on physician supply.

The Data

The 1997 Cap and Its Persistence:

Balanced Budget Act of 1997 capped Medicare GME (Graduate Medical Education) funding - the federal money that pays teaching hospitals to train resident physicians. The cap has remained essentially unchanged for 27+ years.

Only 1,000 new residency slots added in 23 years: Congress approved the first increase in 2020, adding 1,000 slots - the first expansion since 1997

Thousands of qualified medical school graduates don’t match to residency programs annually: They cannot secure residency positions due to the cap, despite being qualified to practice

All U.S. medical school graduates MUST complete residency to obtain a medical license - making the GME cap an absolute bottleneck. Unlike in some countries where medical school graduates can practice with supervision, U.S. licensing requires completed residency.

Current and Projected Shortage:

86,000-139,000 physician shortage projected by 2036 according to the Association of American Medical Colleges (AAMC), the organization representing U.S. medical schools

Only 2% of Medicare GME budget goes to rural training programs despite 18% of the U.S. population living in rural areas - creating a geographic mismatch between training locations and need

Hospitals self-funded 15,000 residency slots over the past 20 years despite the federal cap-proving that demand for training positions exists but federal funding remains frozen. These hospitals train residents without Medicare GME support, absorbing the cost themselves.

Proposed Legislation Has Stalled Repeatedly:

The Resident Physician Shortage Reduction Act would add 14,000 Medicare - supported residency slots over seven years (2,000 per year)

The bill has been introduced in multiple Congressional sessions without passage

Congress revived the bill again in 2025; status remains uncertain

Historical Context: How Professional Guilds Created the Shortage

March 1997 - The Prediction That Went Spectacularly Wrong:

The American Medical Association (AMA) - the professional organization representing physicians - and a consortium of medical organizations issued a joint recommendation to reduce residency positions by 25% (from 25,000 annually down to 19,000).

Their rationale: “The United States is on the verge of a serious oversupply of physicians.”

Congress listened. The Balanced Budget Act of 1997 implemented a cap that effectively froze residency expansion for decades.

The prediction was spectacularly wrong. The U.S. now faces severe shortages, particularly in primary care and rural areas.

2019: The AMA Reverses Course:

The AMA now urges Congress to remove the very caps it helped create. But the damage persists-the 1997 cap remains federal law, functioning as a chokehold on physician production.

Historical Pattern of Supply Restriction:

This is not the first time physician supply has been artificially limited. Through much of the 20th century, the AMA’s control over medical school accreditation-authority delegated by state governments - was used to reduce medical school enrollment and make some graduates ineligible for state licensure. Physician supply has been subject to professional guild control for decades, with predictable effects on physician scarcity and pricing power.

Why This Creates Problems USC Would Solve

Problem 1: Cannot Guarantee Healthcare Access When Training Pipeline Is Capped

When federal law caps the number of physicians who can be trained, and when only 2% of training funding goes to rural programs despite 18% of Americans living rurally, the result is predictable: rural areas, underserved urban communities, and lower - paying specialties like primary care and family medicine face persistent shortages.

Under Universal Standard Coverage, immediate removal of the 1997 cap would be a first-order implementation requirement. You cannot guarantee baseline healthcare access (USC Principle #1) without adequate provider supply. USC would also require reallocation of GME funding to prioritize rural training and primary care rather than urban subspecialties.

Problem 2: Workforce Shortages Force Availability - Based Rather Than Quality-Based Care Decisions

When physicians are scarce, patients see whoever is available, not necessarily the right provider for their condition. Wait times increase. Preventive care gets deprioritized because urgent cases crowd out routine appointments. Rural patients drive hours for specialist care that should be available locally.

Under USC, national standardization of nurse practitioner (NP) scope of practice would immediately expand primary care capacity. Currently, 30 states allow NPs to practice independently, 15 require reduced autonomy, and 11 require physician supervision. USC would establish full practice authority nationwide, allowing NPs to see patients independently for primary care while physician supply scales up. This is USC Principle #5 (Clinical decisions stay clinical) - let qualified clinicians practice at the top of their training.

Problem 3: Outdated GME Funding Rewards Volume, Not Value

Current Medicare GME funding formulas reward teaching hospitals based on the number of Medicare patient-days (hospital days for Medicare patients) and historically funded resident positions-essentially rewarding volume of care and perpetuating existing geographic distribution. This concentrates residency positions in Northeast urban subspecialty programs rather than rural primary care programs where the need is greatest.

Under USC, GME funding would be reallocated to prioritize shortage areas and primary care training, aligning physician supply with population health needs rather than historical funding patterns.

Why Incremental Fixes Fail

The cap is federal law requiring Congressional action:

Despite bipartisan recognition of physician shortages, GME expansion legislation has stalled repeatedly. Medicare GME funding is entrenched in Congressional budget politics, with powerful stakeholders (large teaching hospitals, medical specialty societies) protecting existing funding allocation.

The proposed 14,000 slots over seven years is insufficient:

Adding 2,000 residency slots per year sounds substantial, but medical school enrollment has already increased by more than this, creating MORE unmatched graduates each year if residency slots don’t expand proportionally. The gap between medical school graduates and residency positions is widening, not closing.

Even with immediate cap removal, training takes 3-7 years:

Residency training is three years minimum (family medicine, internal medicine, pediatrics) and seven or more years for surgical and medical subspecialties. Even if Congress removed the cap today and funded 10,000 additional residency positions immediately, those new physicians wouldn’t enter the workforce until 2028-2033. The shortage is immediate; the training pipeline solution is slow.

Immigration pathways remain restrictive despite physician shortages:

International medical graduates (IMGs) - physicians trained in other countries - face U.S. visa caps, lengthy credential verification processes that can take 1-2 years, and state-by-state medical licensing requirements that vary (connecting back to Structural Failure #1: state fragmentation). A physician licensed in Germany or India must complete U.S. residency training and pass U.S. licensing exams even if they practiced successfully for years in their home country.

The structural reality:

The physician shortage is not a market failure - it is a policy-created bottleneck. The solution is not incremental expansion of 2,000 slots per year. It is:

Immediate removal of the 1997 federal cap

Reallocation of GME funding from volume-based formulas to need-based allocation prioritizing rural and primary care

National scope-of-practice standardization allowing NPs and physician assistants to practice at the top of their training

Immigration pathways that recognize foreign physician credentials with appropriate verification

Federal workforce planning replacing guild-controlled supply restriction

THE CASCADE: How Structural Failures Reinforce Each Other

These five structural failures are not independent problems. They form a reinforcing system where each failure amplifies the others:

50-State Fragmentation → Protects PBM Opacity:

No single state has sufficient leverage to demand transparency from PBMs operating nationally. When Illinois and Louisiana sued to recover improperly retained rebates, CVS settled to avoid precedent but continued the practices in 48 other states. When states pass PBM reform legislation, companies create offshore entities (Emisar in Ireland, Ascent in Switzerland, Zinc across state lines) beyond any single state’s jurisdiction. ERISA preempts state regulation for 155 million Americans in employer plans, meaning state-level PBM reform reaches less than half the population.

Employer-Tied Insurance → Creates Captive Markets for Vertical Integration:

When health coverage is tied to employment, workers cannot easily switch insurers based on quality or cost. This job lock creates captive patient populations. Insurers exploit this by steering captive enrollees to affiliated PBMs, affiliated pharmacies, and affiliated physician networks. Patients cannot opt out without changing jobs - and changing jobs means losing coverage.

Fee-For-Service Payment → Drives Over-utilization That PBMs/Insurers Manage Through Prior Authorization:

FFS creates financial incentive for volume. Insurers and PBMs respond by implementing prior authorization-requiring approval before care can be delivered. But PA doesn’t fix the volume incentive; it adds $35 billion in administrative burden (detailed data in the earlier PA discussion) while paradoxically increasing total healthcare utilization through delayed care that leads to complications requiring more expensive treatment.

Physician Supply Constraints → Multiply Through Every Administrative Layer:

Artificial physician scarcity drives up labor costs-doctors command higher salaries when supply is restricted. Those higher labor costs then get multiplied by PBM markups (specialty drugs to treat conditions that weren’t caught early due to primary care access problems), prior authorization administrative burden (adding non-clinical staff costs), fragmented state-by-state billing requirements (requiring administrative staff to navigate different rules), and vertical integration margin stacking (profit extraction at every step of the care chain). When physicians are scarce, health systems have pricing power - and vertically integrated systems extract maximum margin at each transaction.

Vertical Integration Captures Every Step of the Care Chain:

Consider patient “Kate” from CVS’s own investor presentation describing their vertically integrated model:

1. Kate has Aetna insurance (owned by CVS Health-insurer margin)

2. She sees a doctor at Oak Street Health clinic (owned by CVS Health - clinic margin)

3. Doctor prescribes medication; CVS Caremark PBM determines coverage and price (owned by CVS Health-PBM spread and rebate retention)

4. Medication might be manufactured by Cordavis (owned by CVS Health - manufacturer margin)

5. Kate fills prescription at CVS Pharmacy (owned by CVS Health - dispensing margin)

At every step, CVS Health extracts profit. Kate encounters the same company’s margin five times in a single care episode. The system is not designed for care efficiency - it is designed for profit extraction efficiency.

The Compounding Result:

A system where incremental reform in one area gets arbitraged through another dimension. Mandate PBM rebate pass-through → money flows to offshore GPOs instead. Ban spread pricing → profits shift to affiliated pharmacy steering. Reform state insurance regulations → ERISA blocks it for 155 million people. Fix fee-for-service incentives in Medicare → private insurers continue FFS, and providers must operate both systems. Expand residency slots modestly → physician shortage persists because expansion is insufficient.

WHY INCREMENTAL FIXES CANNOT SUCCEED: LESSONS FROM JANUARY 2026

The January 2026 Congressional hearings revealed the sophistication of regulatory arbitrage. Lawmakers from both parties demanded answers about offshore GPOs, vertical integration, and 33% claim denial rates. Executives offered platitudes about “pro-consumer benefits” and disputed data showing their own companies’ denial rates.

The pattern across multiple reform attempts is clear:

Reform Attempted: Require 100% manufacturer rebate pass-through to health plans

Industry Response: Create GPOs (Zinc, Emisar, Ascent) to negotiate rebates; retain money as “administrative fees” before it becomes a “rebate”; PBM technically complies by passing through 100% of what it receives

Result: Same money extracted, different label, technical compliance achieved

Reform Attempted: Ban PBM spread pricing (charging plans more than paid to pharmacies)

Industry Response: Shift profits to affiliated pharmacy steering (68% of specialty drug revenue), GPO administrative fees, and undisclosed “service fees”

Result: Same extraction through different mechanisms

Reform Attempted: State-level prior authorization reform

Industry Response: 10 states pass different PA laws in 2024; multi-state insurers comply minimally in each state with narrow exemptions that don’t reduce overall burden

Result: 50 different state standards, administrative burden fundamentally unchanged, fragmentation increased

Reform Attempted: Antitrust review of PBM-insurer-pharmacy vertical integration

Industry Response: Claim “vertical integration creates efficiencies and lowers costs for consumers”; mergers and acquisitions continue to be approved; market concentration stable at 80% for Big 3

Result: Three companies control prescription drug access for 270 million Americans

Reform Attempted (Announced): Cigna’s “rebate-free” drug pricing model

Reality: Ascent Health Services (Swiss GPO) still negotiates and retains upstream fees; only ~50% of plans expected to opt in by 2028; analysts note this creates more opacity, not less

Result: “Red herring designed to sidestep regulatory scrutiny while maintaining profit drivers” (Economic Liberties Project analysis)

The Structural Lesson:

Sophisticated actors with billions in revenue, expert legal teams, offshore entity domiciliation, and vertically integrated operations WILL game incremental reforms. They will technically comply with the letter of new regulations while maintaining profit extraction through restructured mechanisms. They will create new labels for old practices. They will sue states to block oversight under FOIA. They will domicile negotiating entities in Ireland and Switzerland. They will construct temporary walls inside existing buildings and call it a separate company.

You cannot regulate your way out of a structure designed for complexity and opacity.

THE USC ALTERNATIVE: Why Structural Replacement Works Where Incremental Reform Fails

Universal Standard Coverage eliminates the structural mechanisms that produce these failures. Rather than trying to regulate behavior within a broken architecture, USC proposes replacing the architecture itself.

How USC Would Address Each Structural Failure:

Why USC Succeeds Where Reform Fails-Three Structural Advantages:

1. Eliminates Arbitrage Opportunities:

No state-by-state variation to exploit (single federal system applies nationwide)

No offshore entity stratagem possible (federal law, federal enforcement, single negotiating entity)

No PBM intermediary to game (direct federal negotiation with manufacturers, direct pharmacy payment)

No insurer-PBM vertical integration to create (single federal payer eliminates the multi-payer structure that enables vertical integration)

2. Removes Extraction Layers:

No private insurance company margin (single federal payer)

No PBM spread pricing, rebate retention, or GPO administrative fees (no PBM intermediary)

No prior authorization administrative tax - $35 billion eliminated (no PA required for medically necessary baseline care; PCP-led care coordination replaces insurance-clerk gatekeeping)

No billing complexity multiplied across dozens of payers with different rules (single payer, automated payment rails, standardized claims)

3. Aligns Financial Incentives With Health Outcomes:

Primary care capitation rewards preventing disease, not treating late-stage complications

National rate card eliminates financial steering to affiliated high-margin providers

No PA denial quota driving care delays (no financial incentive for payer to deny necessary care)

Federal workforce planning allocates training resources to shortage areas rather than protecting guild-controlled scarcity

Closing Regulatory Loopholes Structurally, Not Through Rules:

When the problem is offshore GPOs retaining manufacturer rebates under the label “administrative fees,” the solution is not better disclosure rules (which can be gamed)-it is eliminating the rebate negotiation structure entirely by having the federal government negotiate drug prices directly and transparently.

When the problem is vertical integration allowing margin stacking at every care touchpoint (insurer → PBM → pharmacy → clinic all owned by same parent company), the solution is not breaking up companies (which reconsolidate through M&A within a decade) - it is eliminating the multi-payer structure that creates financial incentive for vertical integration and captive patient steering.

When the problem is 50-state regulatory fragmentation, the solution is not “better interstate coordination” (which has failed for decades) - it is federal preemption establishing one national standard.

CONCLUSION: From Incremental Fixes to Structural Replacement

The U.S. healthcare system produces $5.3 trillion in annual spending, 27 million uninsured Americans, $220 billion in medical debt, 20.6% medically unnecessary care, and approximately $1 trillion in administrative costs-not because Americans are sicker than people in other wealthy countries or because healthcare companies are uniquely greedy.

These outcomes are produced because the architecture rewards complexity, punishes transparency, and protects inefficiency.

Fragmentation across 50 state regulatory regimes creates opportunities for regulatory arbitrage-companies domicile entities offshore and shift practices across state lines to evade oversight. Employer-tied insurance creates captive patient populations and job lock that prevents market discipline. Fee-for-service payment drives unnecessary volume and $45.6 billion in defensive medicine. PBMs profit from deliberate opacity, creating offshore entities to retain billions while technically complying with rebate pass-through mandates. Artificial physician supply constraints - a 27-year-old federal cap that the AMA lobbied for when warning of “physician oversupply” - create provider scarcity that multiplies through every layer of the system as higher labor costs, longer wait times, and geographic maldistribution.

Each structural failure reinforces the others. Each incremental reform gets gamed, evaded, or arbitraged through another dimension of the system. Each Congressional hearing produces testimony and promises, not structural change.

The January 2026 hearings were not the first time lawmakers demanded accountability. They will not be the last.

CVS, UnitedHealth, and Cigna will continue to own insurers plus PBMs plus pharmacies plus clinics plus offshore GPOs. They will continue to report 4-7% profit margins on their PBM operations while capturing 68% of specialty drug dispensing revenue through affiliated pharmacies. They will continue to claim their vertical integration produces “pro-consumer benefits” even as they create temporary walls inside existing buildings and call the space behind the wall a separate company to technically comply with rebate pass-through requirements.

Unless the operating system is replaced.

Universal Standard Coverage is not an incremental fix. It is not a transparency mandate, a tax credit, a public option, or a state-level experiment. It is structural replacement of a system designed for complexity with a system designed for the opposite goal:

One federal system with one set of rules-not 50 state systems plus ERISA preemption creating regulatory voids

Healthcare as a baseline guarantee independent of employment-not an employment benefit that disappears when jobs change

Payment models that reward health, not volume-primary care capitation and national rate cards, not fee-for-service incentivizing unnecessary procedures

Transparent direct negotiation-federal formulary development with published prices, not opaque PBM intermediaries with offshore GPO retention schemes

Federal workforce planning-immediate removal of the 1997 residency cap and national NP scope standardization, not guild-controlled supply restriction

Clinical decisions guided by physicians and evidence-based guidelines-not insurance company prior authorization clerks with denial quotas

The current system cannot be reformed into efficiency through incremental fixes. The structure itself must be replaced with architecture designed for frictionless access to medically necessary care, $0 at the point of care for baseline services, clinical decisions staying with clinicians, and one national standard that applies to everyone.

Next: The architecture of a system designed to work - Universal Standard Coverage in detail. (coming soon)